How Your Deposits Are Protected

When it comes to your savings, peace of mind matters. That’s why deposit insurance is built into both banks and credit unions in Canada—at no cost to you. This insurance is applied to most types of deposits, including chequing and savings accounts as well as GICs.

But there are some important differences in how that protection works.

At a Bank

If you bank with a traditional bank, your insurable deposits are insured by the Canada Deposit Insurance Corporation

• Up to $100,000 per category, per institution

• Coverage applies across categories like personal accounts, joint accounts, and registered plans

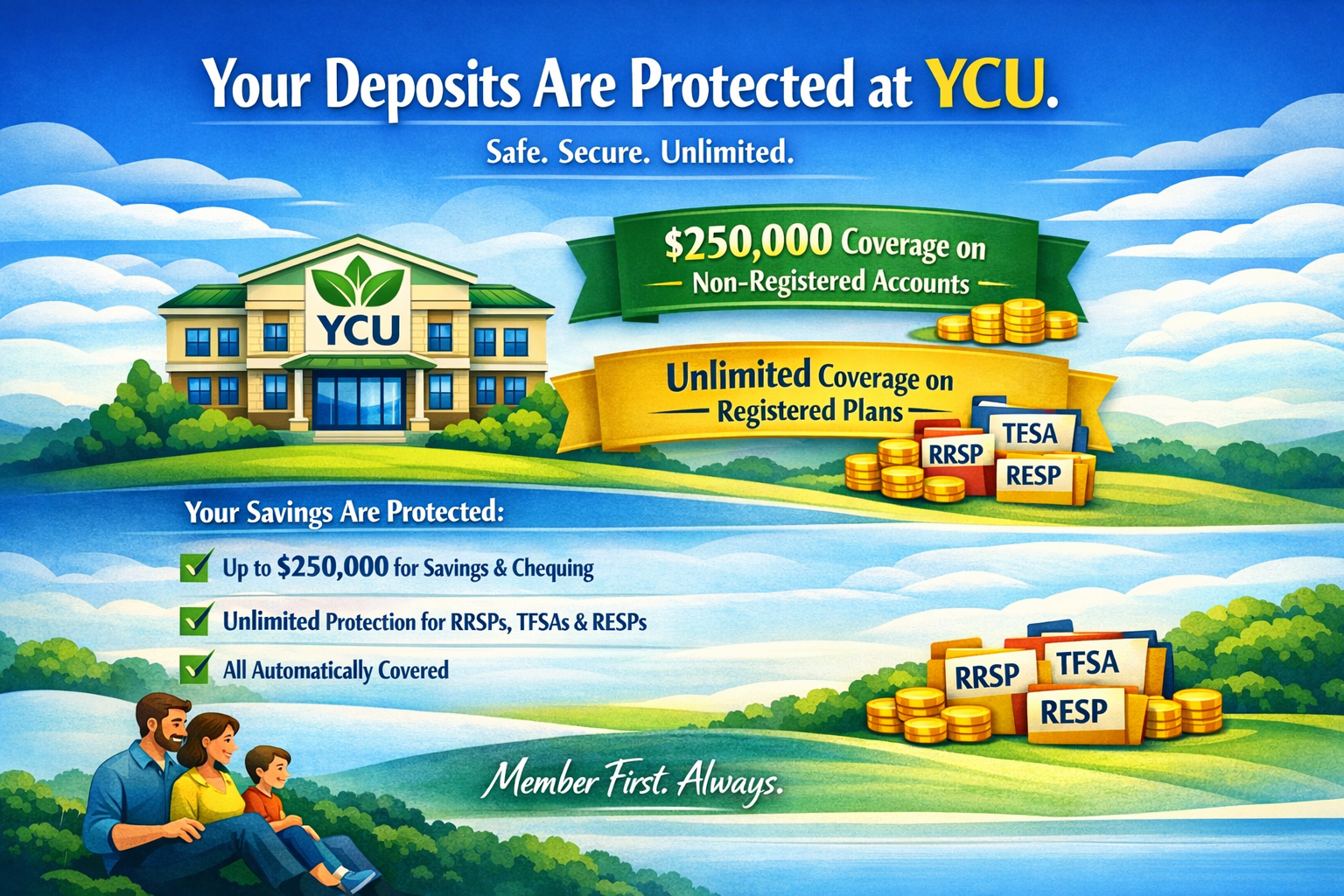

At YCU

As a credit union member in Ontario, your insurable deposits* are protected by FSRA:

• Up to $250,000 on non-registered accounts like chequing and savings accounts or non-registered GICs

• Unlimited coverage on eligible deposits in registered accounts like TFSAs and RRSPs and others

What This Means for You

Both systems keep your money safe—but credit unions offer:

• Higher coverage on non-registered accounts

• Unlimited protection for your registered account savings

It’s a simple, strong safety net—so you can focus on what matters most.

Member First. Always.

At YCU, protecting your deposits is just the beginning. As a member, you’re part of something bigger. A local financial institution built around your needs, your goals, and your community.

Have questions about your coverage? Check out the following short video from FSRA:

Protecting Credit Union Member Deposits: What's Covered and What's Not Covered

Or look up the FSRA website at:

Credit Unions and Deposit Insurance | Financial Services Regulatory Authority of Ontario

* Insurable Deposits include chequing and savings accounts, GICs, money orders, funds-in-transit and index-linked term deposits (principal portion only.) They do not include mutual funds, membership shares, investment shares or foreign currency deposits.